Where to Invest Your Money Today (The Employee vs. The Entrepreneur)

Do you have a framework for your finances?

Do you have a framework for your finances?

Do you know the ABSOLUTE BEST place to invest your money?

You will after today.

Today, I am sharing a financial framework I use to simplify my decisions with money.

There’s a lot of FOMO in finance.

But, if you are an entrepreneur, there shouldn’t be.

I am getting ahead of myself, first, a story.

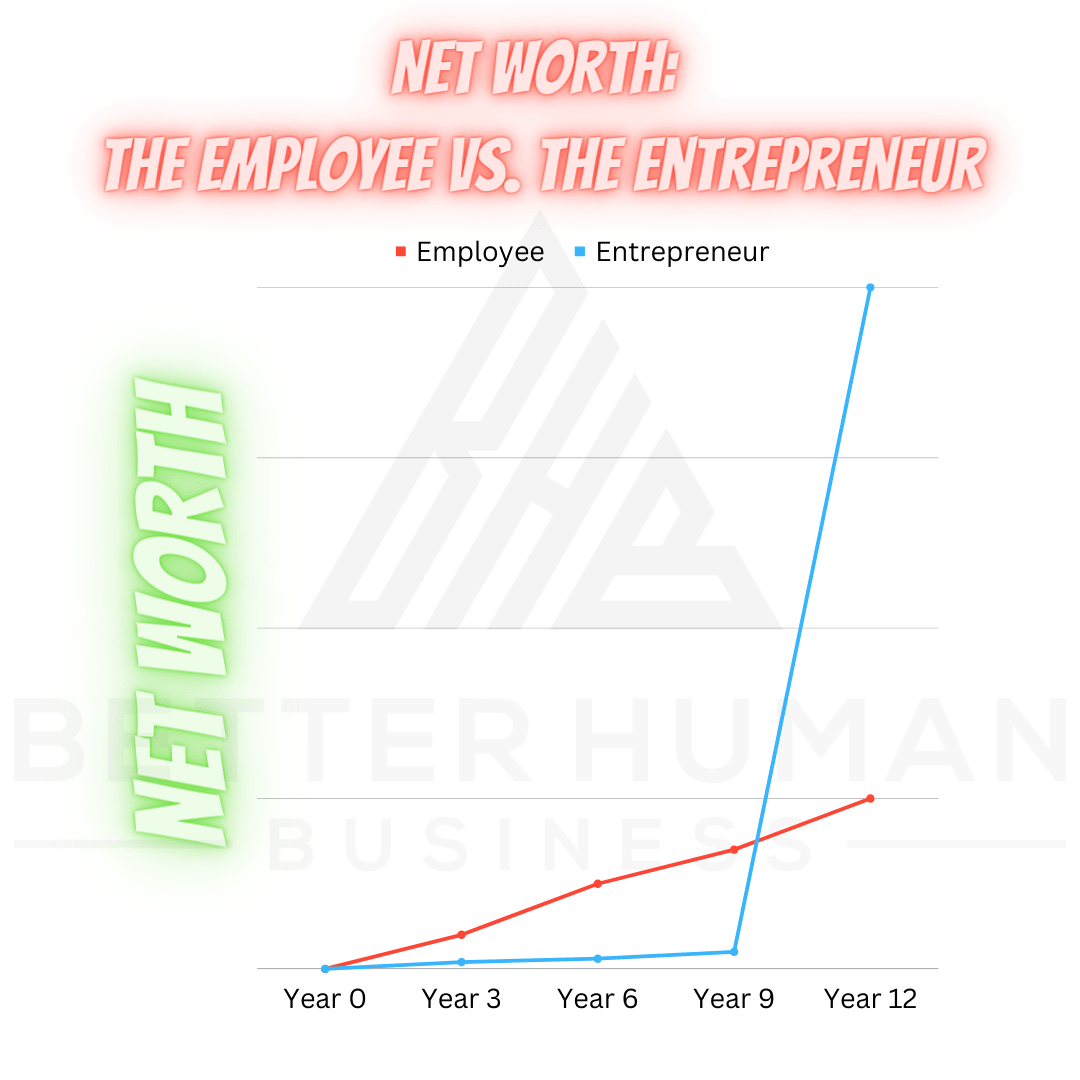

The Employee vs. The Entrepreneur

I have a friend I’ve known for a long time who is nearly perfect regarding money.

I mean, he budgets, he saves, he invests.

He DOES NOT make financial mistakes. He DOES NOT have debt.

Literally, perfect.

When we were both employees, I thought it would be impossible to surpass him. He was just on a different level.

I wanted to be smart with my money, but I still wanted to enjoy life.

Then, our paths diverged.

He remained an employee.

I became an entrepreneur.

I kept in touch with him, and we’d chat on the phone once or twice a year. I’d ask what he was doing for investing and learn of something new he was up to or how well his investments were doing.

When he would ask me, I didn’t have much to say. My wife and I spent every dime we could save the first couple of years of marriage to get out of debt. After that, I was sinking money into my business, not investing.

This went on for a long time…

Then, something magical happened. All the money I was dumping into business courses, business masterminds, and advertising started to work. I began to gain skills; I was getting good at being an entrepreneur. Things started to compound.

He had gotten good at being an employee.

So what happened?

I was able to leapfrog the investments he had been working on for a decade in less than two years. Not to mention, my business is a sellable entity with value.

Overnight success?

Sure. Fifteen years to an overnight success.

Now, when we chat, he’s asking me about business and wants to start one of his own.

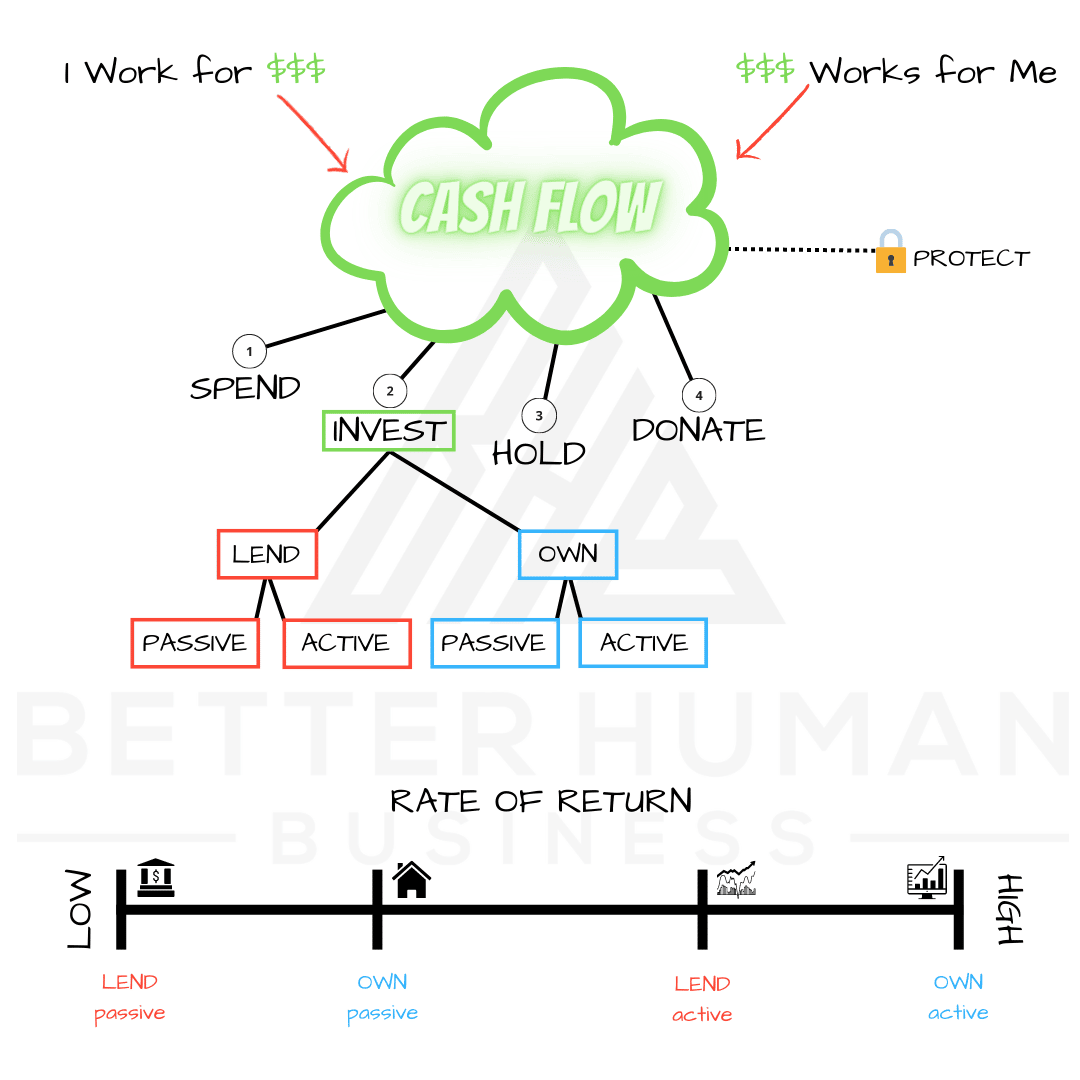

A Simple(ish) Money Model

Today, I’ll break down a financial framework that will demystify the complexity of finance. I will be referring mainly to the graphic above. But, in the end, you’ll ask yourself, “Is it that simple?” And the answer is: YES.

So let’s talk about money. Because you can be an entrepreneur, make a ton of money, and still suck with your money. Most do.

Before that, the legal stuff.

Disclaimer: I am not a financial advisor. Do not take anything in this newsletter as financial advice, ever. Do your research. Consult a professional investment advisor before making any investment decisions! My articles are for entertainment only!

Now, on with it!

Let’s Start with CASH FLOW.

Cash flow is simply the money you have coming into your possession. For example, you can have cash flow from your work (I Work for $$$), or you can have cash flow from an investment ($$$ Works for Me).

Next, PROTECT.

You have to protect your cash flow. You protect your cash flow through insurance. You need adequate insurance in the following categories: disability, health, life, home/property, and auto. Not much can screw up your financial life more than being underinsured when an unfortunate event occurs outside of your control.

Now, WHAT TO DO with your Cash Flow.

With your Cash Flow, you can only do four things:

- SPEND: We all know how to spend money. Buy what you need before you buy what you want, and keep the most important rule: Only spend what you have.

- HOLD: You can hold your money, a.k.a. save it. The general rule here: save enough for 3-6 months of living expenses.

- DONATE: You can and should donate your money. How much and to what cause is a personal preference.

- INVEST: Everyone’s favorite… Investing your money. I will not tell you where to invest your money, but I will give you a framework for investing it.

When you Invest, you are either LENDING your money to someone, and they are paying you for lending it to them. Or you are putting money into something to OWN, which will generate cash flow.

Once you realize that’s all you can do with your money in investing, it gets uncomplicated fast.

Within this LEND/OWN framework, there is a PASSIVE or ACTIVE option. Each option generates a different rate of return.

Anything PASSIVE will generate a lower rate of return. If you don’t want to work, the return will be lower. Generally, the risk is also lower.

Examples:

- LEND (passive): Certificates of deposit (CDs). You LEND money to a bank for a set time; they give you a small return for lending them the money.

- OWN (passive): Real estate. If you OWN your home, it is appreciating while you do nothing. You could also OWN a house and let someone else rent it out, and you get cash flow. Being a landlord is not entirely passive, but it’s a lot less active.

NEXT, ACTIVE Investments.

Anything ACTIVE will generate a higher rate of return. If you put in the work, the return will be higher. But, generally, the risk is also higher.

Examples:

- LEND (active): Trading. You can trade stocks or crypto; it’s all the same. I’m not talking about putting all your money in an index fund and waiting 30 years. Instead, I mean active day trading, a high-yield activity (when you’re good or lucky). You LEND your money to an entity that uses your capital to attempt to improve its value.

- OWN (active): Business. Owning and being active in a business has the highest rate of return you can see. Nothing can beat it.

My take:

If you are NOT an entrepreneur, by all means, dive deep into CDs, bonds, real estate, stocks, and crypto.

I mean, how else are you going to make more money?

If you ARE an entrepreneur, go all in on your business!!

Forget about all that other stuff until you have so much money you are forced to start figuring out where to put (invest) it.

Oh, and try harder.

-JM